Are Investors With Good Credit Getting Punished?

“Biden to hike payments for good credit home buyers to subsidize high-risk mortgages” is the headline of the article that caught the internet by storm. How does this impact you as a real estate investor that pays their bills on time? I have seen comments that state “I am going to miss a few payments before applying for a loan so they can get a better interest rate.” Hold on just a second, let’s dig into this a little before implementing that strategy.

Changes To Fannie Mae And Freddie Mac Pricing Models

In January, Fannie Mae and Freddie Mac changed their pricing model to help serve a broader community and promote home ownership. The changes hit the Loan-Level Price Adjustment (LLPA) which is used to compensate Fannie and Freddie for riskier loans. You will see a higher LLPA for an investment property, with a small down payment and a low credit score for example. These changes were implemented on any loan delivered to Fannie or Freddie as of May 1, 2023, which is why this hit the web like it did in April.

Loan-Level Price Adjustment (LLPA)

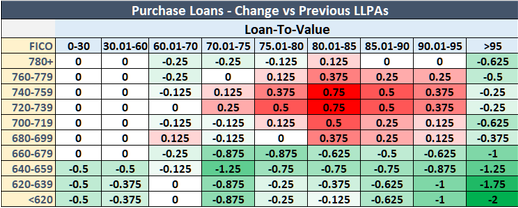

The LLPA is a fee charged by Fannie or Freddie that is paid by the lender and often passed to the borrower in the way of a higher rate. You can see in the chart below, which I copied from Mortgage Daily News, the changes to the previous pricing. The best I can tell from looking at multiple lender rate sheets, a 1 LLPA is close to a .5% change in rate for most lenders. In an example, if you have an LLPA of 3 and a par rate of 6%, your mortgage rate would be close to 7.5%. This will vary depending on lender.

The green are improvements from the previous pricing model. Although this is the chart getting the publicity, it is important to note this chart does not show the LLPA fee, it is the change to the previous fee. You can see clearly that the idea is to help lower credit score borrowers with higher LTVs while higher credit quality borrowers with more reasonable LTVs pick up the tab. This chart shows us that a 720 or higher credit scores with 20% down payments is the target for the price adjustment while the 640 and lower credit scores and lower down payments are the beneficiaries. This is why people are so upset.

When you look at this the hair on your arms might stand straight up like mine did and is why we got headlines like the one I opened the article with. It seems completely unfair to penalize someone that pays their bills to help the ones that don’t. This is exactly how 2008 came to fruition. With that said, I would not stop making payments on your credit cards just yet!

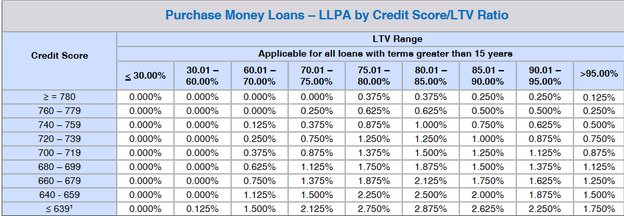

This chart, which I pulled directly from Fannie Mae, shows the amount the fee will be after the changes.

Bottom Line: Borrowers With Higher Credit Scores Will Be Paying More

You can see that, for the most part, the higher risk loans still pay a higher fee, but it is not as lopsided as it once was. I still find it interesting that the person with a sub 640 credit score will pay less with a greater than 95% LTV than someone with the same score putting 20% down. Or how the person with a 699 credit score and 20% down pays more than the person with a 640 credit score and only 5% down. Maybe that is something I can try to understand on a different day.

In any case, although the headlines are true and higher credit score borrowers will be paying more than they once did and that money will be shifted to help the riskier borrowers pay less, it does not mean that riskier borrowers are now paying less than low risk borrowers. Keep making those credit card payments.